This post explores aspects of CEP’s latest research findings, weaves in data from five other new research reports, and concludes with suggested — and urgent — action steps. Spoiler Alert: Those steps entail mitigating the challenges to foundations and nonprofits alike created by the new tax law, building the capacity to fend off future threats, and helping the 501(c)(3) community cope with the newly disrupted reality under the new law.

Quick Glimpse: CEP’s Research Findings

The latest research brief by the Center for Effective Philanthropy, Bracing for a Downturn: Nonprofits, Charitable Deduction Worries, and How Foundations Can Help (co-authored by Kevin Bolduc and Ellie Buteau), shares results of a survey asking foundations and nonprofits two similar questions about the anticipated effect of the new federal tax overhaul law.

The first question asked whether the respondent was concerned about potential decreases in charitable giving by individuals. Fewer than one out of five respondents (19 percent of foundations, 14 percent of nonprofits) indicated they were not concerned about a potential decrease in charitable giving. More than four out of every five foundation and nonprofit leaders surveyed voiced either concern or uncertainty about the new tax law’s impact on charitable giving.

The second question asked those who reported concern or uncertainty what they thought foundations can do (other than to make more or larger grants) to help grantees respond to the new tax law. When reviewing responses to this open-ended question, CEP researchers documented several themes. The most consistent response was that foundations could support nonprofits’ “capacity to respond” (39 percent of foundations and 33 percent of nonprofits).

The greatest divergence in views? More than a third (36 percent) of nonprofits thought foundations could, as one respondent wrote, “help counteract any decline in giving [by] endorsing the value of nonprofits, the importance of their work, and the needs of their beneficiaries.” Apparently nonprofits, believing that foundations are respected voices that can speak up for the work of nonprofits without appearing self-serving, wish foundations would inspire individuals and corporations to increase their contributions to nonprofits. The research brief quotes one nonprofit leader: “Educate the general public that support is crucial for nonprofits and that without their support many services that assist those who live in poverty or disabled will not be able to continue.”

In contrast, not a single foundation identified that as an option.

But what I found most striking in the research findings was what was missing.

The Silence Speaks Loudly

Occasionally, silence is more powerful than words. And CEP’s research has served the entire 501(c)(3) community well by effectively recording the deafening silence from foundations and nonprofits on a most urgent matter.

The genesis of the survey was a once-in-a-generation tax overhaul bill that threatens to severely harm the work of the 501(c)(3) community. Yet when CEP’s researchers reviewed the open-ended responses to identify categories of the “most common role foundation funders can play to support nonprofits in response to tax legislation,” the absence of responses didn’t justify creating a category for “supporting the advocacy work needed to limit the harm from the new tax law.” Either no one, or not enough respondents, spoke up to say, “Let’s fix what policies we can in the tax law and prevent future policy debacles.”

That bewildering collective silence brings to mind the quote sometimes attributed to Albert Einstein: “Insanity is doing the same thing over and over again but expecting a different result.”

How can the 501(c)(3) community expect different policy results if we continue to ignore the urgent need to protect our common interests through defensive policy work? That’s not an academic question. Right now, serious policy threats loom over foundations and nonprofits and demand immediate and aggressive pushback. Just look at the aftermath of the tax overhaul bill and the urgent need to engage in advocacy at both the federal and state levels.

At the federal level, defensive policy battles are being waged by a few on behalf of all. The new tax law contains significant drafting errors and punitive measures that expose charitable nonprofits, houses of worship, and private foundations to new — and unknown — tax liabilities. (For examples, see this initial letter the National Council of Nonprofits submitted to the Treasury Department and IRS outlining confusion and concerns about new unrelated business income taxes on certain employee fringe benefits and on each undefined separate “trade or business.”)

Meanwhile, state governments are reopening their tax codes to conform (or not) with the new federal tax laws. Whenever a government opens its tax code, there will be winners and losers. Do foundations and nonprofits trust that corporations wanting to lower their taxes and state and local governments hungry to raise new revenues will put aside their own self-interest to hold charitable nonprofits and foundations harmless? Have we not learned from past experiences — over and over again?

Here’s just one current example. Vermont is in the process of spending its tax law “winnings” by lowering corporate and individual tax rates, while also repealing the state charitable deduction and replacing it with a much smaller tax credit. These moves will only shove more demands onto nonprofits delivering services in the community while choking off charitable contributions, all with the unspoken expectation by policymakers that private philanthropy will fill the resulting financial gaps.

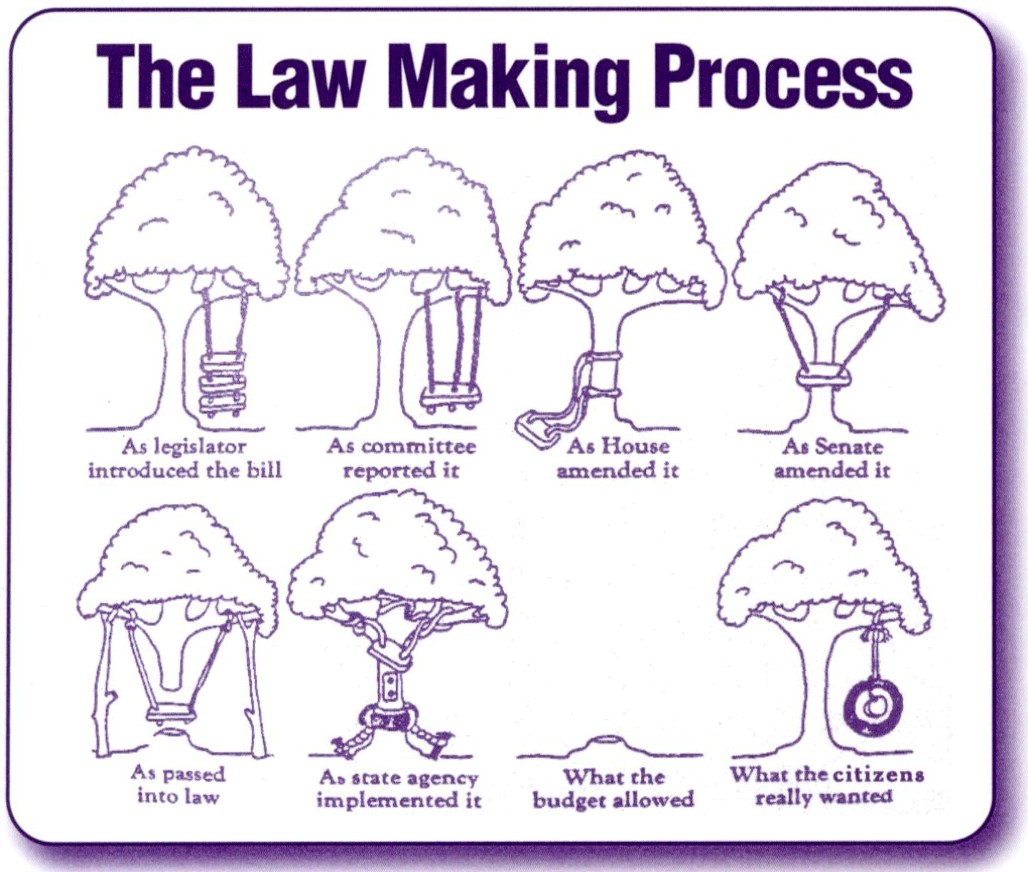

The image below, once commonplace in legislative chambers across the country, can serve as a concrete reminder to all foundations and nonprofits that the public policy process continues long after legislation passes.

The 501(c)(3) community has multiple opportunities right now to protect itself and those we serve. The community cannot afford to ignore these continuing threats. Foundations need to invest in defensive policy work to protect the common good of the sector just as much as they invest in the various proactive policy initiatives they support. Without a safe policy environment, all foundations and nonprofits are exposed to threats to their missions through government interference, imposition of new taxes and fees, restrictions on giving incentives, and more.

Concerns about Charitable Contributions

When passing the tax overhaul bill late last year, Congress eliminated and limited many longstanding and popular deductions, but it did not change the statute allowing individuals to claim a deduction for their charitable contributions. Congress did, however, change other laws that may affect charitable giving, such as almost doubling the standard deduction and doubling the exemption from the estate tax. That explains why more than half of the funders and nonprofits that CEP surveyed (53 percent of each group) expressed concern “about a potential drop-off in individual donations in the wake of the tax legislation.”

As noted in Bracing for a Downturn, “the actual effect of the legislation on future charitable giving remains unknown” (emphasis added). While the precise dollar amounts may be unknown, the following data clearly point in one direction: downward. The only questions are: by how much and which organizations (and the people they serve) will lose the most?

1. How much will charitable giving shrink?

- Roughly $21 billion in charitable giving will be lost every year as a result of the doubling of the standard deduction, according to economists with the Tax Policy Center who project that the number of households claiming an itemized deduction for charitable contributions will fall by about 21 million in 2018. (It is well known that most people give for the mission but give more because of the tax incentive. Eliminate the incentive and the “more” goes away and giving patterns change. Personally, I don’t believe individual giving will drop the full $21 billion in 2018, because most taxpayers will need to complete their tax returns a couple of times to discover the full implications of the combined federal and state tax law changes. It may take a year or two before individual giving reflects the effective loss of the incentive for about 94 percent of taxpayers; a century-old habit is hard to break. I hope.)

- Another $7 billion in contributions will be lost annually because of the almost doubling of the exemption to the estate tax, according to scholars at Indiana University.

- “Historically, giving has always declined the year after a major tax law change,” observes Larry Raff. Why? Because when people see that tax rates will go down the following year, they can claim a larger tax deduction when rates are higher, so they increase their gifts before the lower rates go into effect. “Many donors doubled up gifts in 2017, so 2018 will be softer” in terms of donations. That’s certainly reinforced by fresh data just released by the Fundraising Effectiveness Project (FEP) showing sluggish giving in the first quarter of 2018 compared against the same period in 2017. The comparison “reveals that every metric the FEP analyzes in on the decline — with [one] exception.” “The bottom line is that we are now in a very different charitable landscape than we were 12 months ago,” according to one person looking at the fresh data.

Those experts and others project significant losses in individual giving (and I’m unaware of a single study suggesting that giving might increase). Yet some wildcards are hidden up the sleeve that could change things. On the positive side, higher payouts from private foundations this year due to the banner year for the stock market in 2017 should help mitigate losses in individual giving (but certainly not by $28 billion). On the other hand, Americans’ fears about personal disposable income could negate my hope that the decline in giving will be delayed a year or two. Likely culprits sparking fears include property tax bills (people know the new tax law caps their federal deduction for state and local taxes at $10,000), large increases in medical insurance premiums this fall (due to the undercutting of the Affordable Care Act), or other external events. Also, the true extent of the decline could be masked on paper by any mega-gift(s) from billionaire(s), although the gaping holes in local nonprofit budgets would remain.

2. Which organizations — and people — will lose?

The projected annual loss of $28 billion in charitable donations will not be spread evenly across all nonprofits. Income inequality is “play[ing] out in our sector: nonprofits serving the wealthy continue to amass resources, while those serving communities in need are barely getting by,” Heather McLeod Grant, Adene Sacks, and Kate Wilkinson of Open Impact write in The New Normal: Capacity Building During a Time of Disruption, a research report published last month.

The New Normal researchers found that “donors who will still itemize (in the top 5 percent of income) ‘tend to focus their giving on large institutions like universities and hospitals.’” Meanwhile, community-based organizations meeting local needs, the “smaller social-service and safety-net nonprofits, [will be hit] harder than larger endowed institutions, which have a financial cushion and access to donors.” They note the sad irony that “despite a renewed focus on issues of power, equity, and race in the social sector, these issues are playing out among nonprofits and reflected in which ones are capturing new funding.”

Large nonprofit institutions will continue to enjoy largess and can simply hire more development staff. In contrast, the tax law changes and other disruptive forces make it even more difficult for local small to mid-sized community-based nonprofits, such as the local food bank, community theatre, and rural healthcare clinic, to survive, let alone thrive. Consequently, the nonprofits on which the public relies every day will be further constrained in meeting their missions.

Why a Loss of Charitable Giving Hurts More Now: Fresh Data about Increasing Public Need

Three other new reports reinforce why respondents to the CEP survey expressed concerns about potential declines in charitable giving.

- ALICE Report, United Way (May 2018). “There are 8 million U.S. households that can’t afford a basic monthly budget including housing, food, child care, health care, transportation, and a cell phone, according to new data released by the United Way ALICE Project.” That’s 43 percent of all households in the U.S.

- Human Needs Index, Salvation Army and Indiana University Lilly Family School of Philanthropy (May 2018). “A decade after the Great Recession, the Human Needs Index reveals that despite an improving national economy,” about “three-quarters of states show higher levels of need in 2017 compared to 2007.” (Emphasis added.)

- State of the Nonprofit Sector 2018, Nonprofit Finance Fund (May 2018). Survey responses from “almost 3,400 nonprofit leaders across all 50 states and a wide range of sizes and missions” report, among many other things:

- 86 percent say demand for services keeps rising, and 57 percent say they can’t meet it.

- 66 percent say offering competitive pay is a top challenge, and 59 percent say they are finding it hard to employ enough staff.

- 62 percent say financial sustainability is a top challenge, as is full-cost funding for 57 percent.

The data are irrefutable — adverse public policy actions continue to pile on more work and drain more resources. The bottom line? Nonprofits cannot continue to do so much more for so many more for so much longer with even less.

Conclusion: Urgent Action Steps

Since Prometheus stole fire and gave it to humanity, fire has had the capacity both to harm and to do good. The 501(c)(3) community has been burned in the public policy arena, repeatedly, by ignoring threats and assuming that other policy players will voluntarily set aside their self-interests to be nice and fair to us.

Can we learn from those experiences to light a fire behind investing in and developing a robust defensive policy shield for the collective good? We must. Otherwise, we will remain stuck in the vicious cycle about which George Santayana warned: “Those who cannot remember the past are condemned to repeat it.”

Foundations — both for themselves and for their grantees — need to invest in defensive policy work to protect the common interests of the 501(c)(3) community at the federal and state levels. They must do this both to help unravel the current debacle from the new tax law and to prevent the next policy disaster from blocking advancement of mission priorities.

Community-based nonprofits need to focus efforts where action can do the most good:

- We all must block the latest attempt (launched two weeks ago, following several attempts last year) in Congress to politicize the 501(c)(3) community by passing anti-Johnson Amendment language.

- We all must convince the Treasury Department and IRS to immediately and officially delay implementing the new UBIT provisions until a year after they release controlling guidance to provide a reasonable transition period for foundations and nonprofits to develop the necessary record-keeping systems.

- We all must engage at the state level where legislatures regularly try to pass laws seeking to tax the property and other assets of foundations and nonprofits and interfere with our independence.

In this time of rapid disruption, this wisdom captured in the CEP research brief warrants emphasis: “Funders need to stop doing the same old thing: convening people, writing papers, doing research. Stop and rethink the model. … One funder we know created a rapid-response fund and then asked nonprofits to prove their impact, using the same methods as their traditional grantmaking.”

Finally, a large percentage of nonprofits responding to the CEP survey expressed a desire for foundations to educate their grantees about the new tax law. For foundations seeking to help your grantees in this way, please know you can point them to the free materials on the National Council of Nonprofits website that we have collected, developed, and curated for the good of the sector: Resources on How the New Federal Tax Law Impacts Charitable Nonprofits.

Tim Delaney is president & CEO of the National Council of Nonprofits.

Bracing for a Downturn: Nonprofits, Charitable Deduction Worries, and How Foundations Can Help is available for free download here.